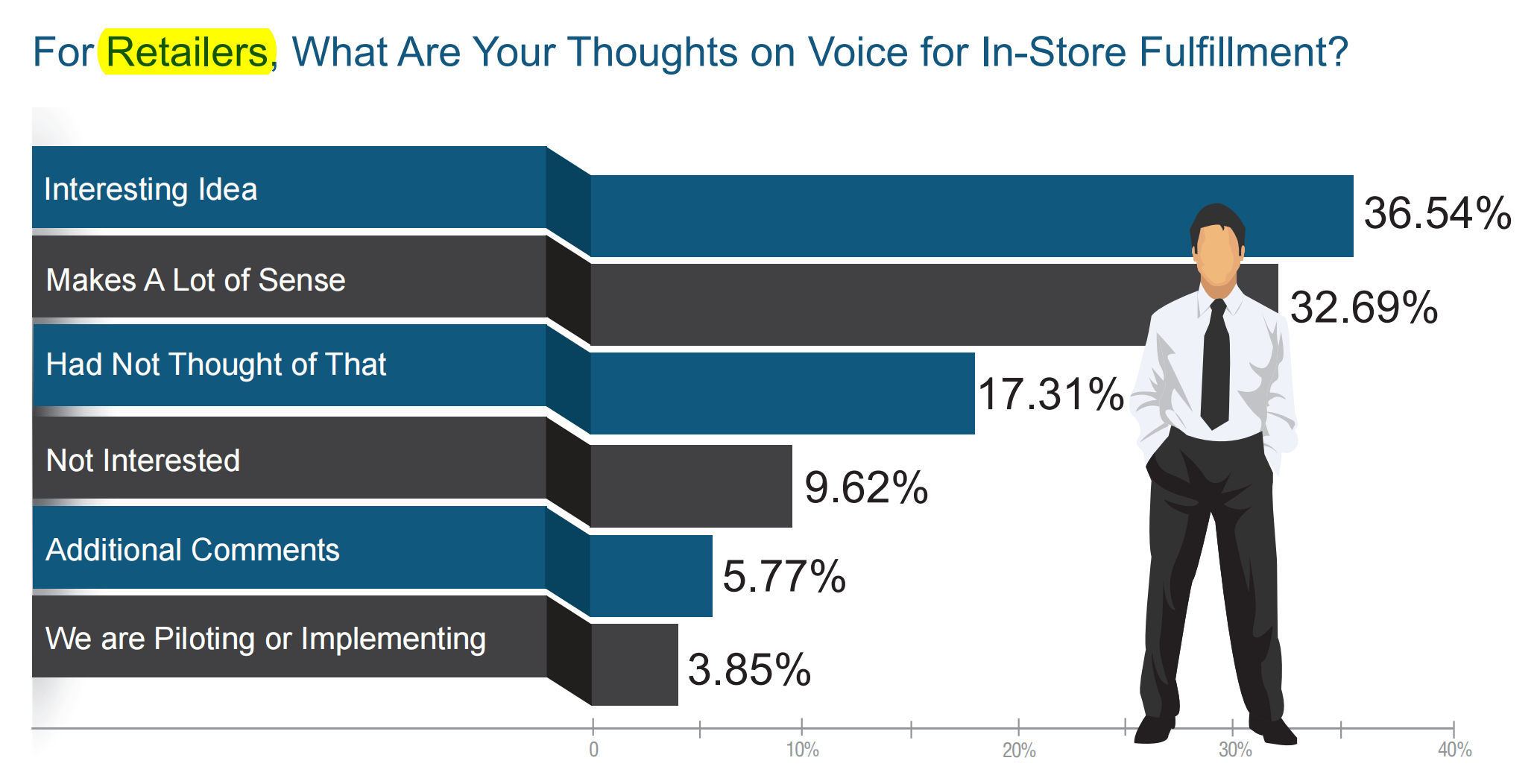

Will voice picking technology trend continue to climb?

There are multiple technology options available in the market. Some technologies have been around for more than 20 years, such as RF scanning, Sorting and Pick-to-Light.

Meanwhile, more advanced technologies like RFID and Robotic Picking which look promising are still in infancy stage.

Voice technology is positioned in between. In the past 10 years, there has been significant adoption in the market, especially in Picking, which is also our focus here.

How could a user decide what is the "best fit" among these options? How to balance the trend, internal needs and challenges? Could the emerging Voice technology be the choice?

In search of solutions, SCD has conducted a study in early 2014 through a group of 155 respondants.

The particpants encompassed a broad range of industries and enterprises.

The respondants came from multiple industry verticals where the majority are represented by Retail (15.8%), followed by Third Party Logistics [3PL] (12.6%), FMCG (11.5%) and Wholesale/Distributor (9.75%). There was no difference based on business size except that businesses below USD 100 million are less likely to adopt existing technology.

The study also implies the complexity of a DC does not depend on its business size. For instance, a USD 300 million dollars consumer goods company using one type of device for its operation has a higher complexity than a USD 1 billion dollars company of pallet-pick operation using 10 robotic units.

Survey Outcome

The respondants were first asked to rate their main challenges and objectives, between 1 and 7, where 1 being the highest. Operating cost reduction stood out being the top, followed by productivity improvement.

However, "Labour Management" and "Capability improvement in onmi-channels" remain "low challenges". The latter was below the median value (3.5).

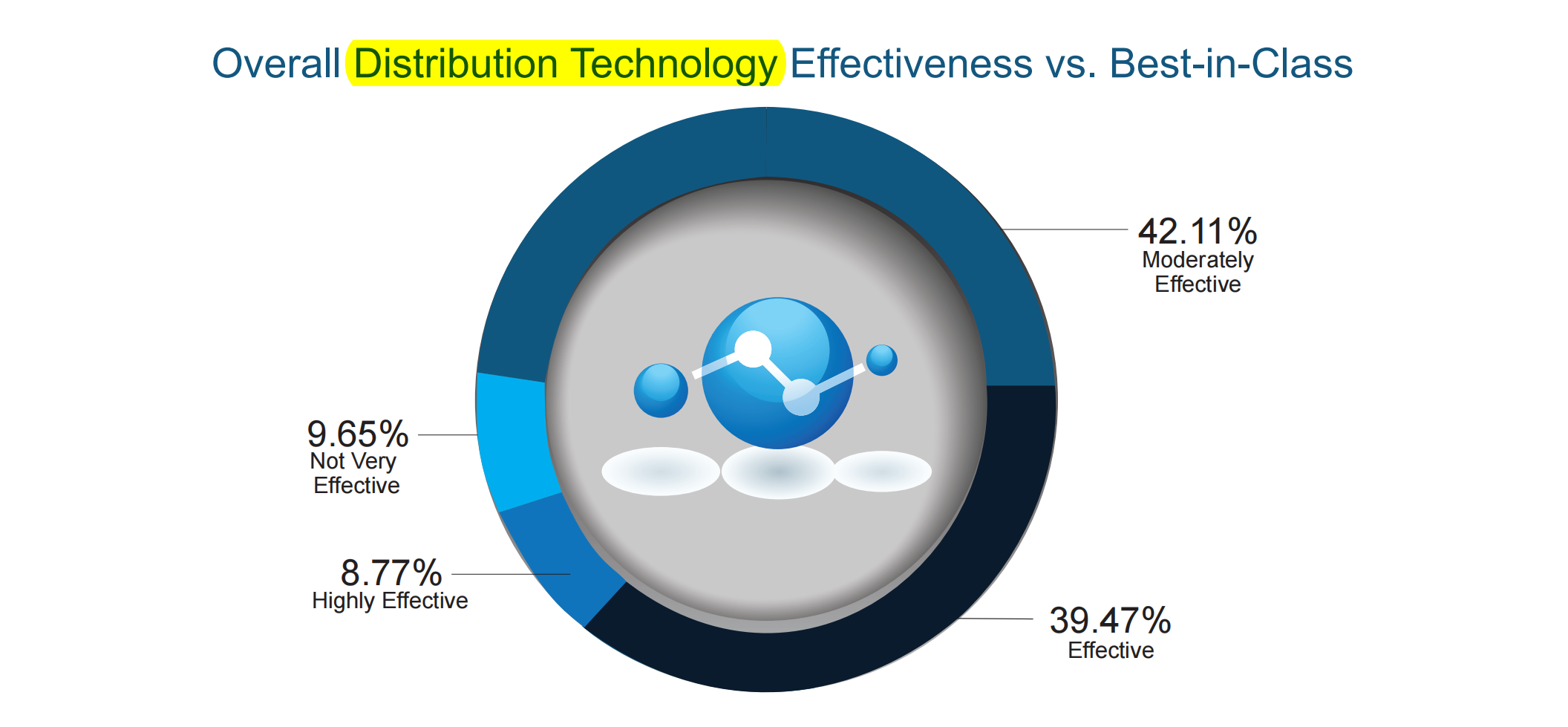

The study also requesetd respondants for a self-assessment of their own DCs.

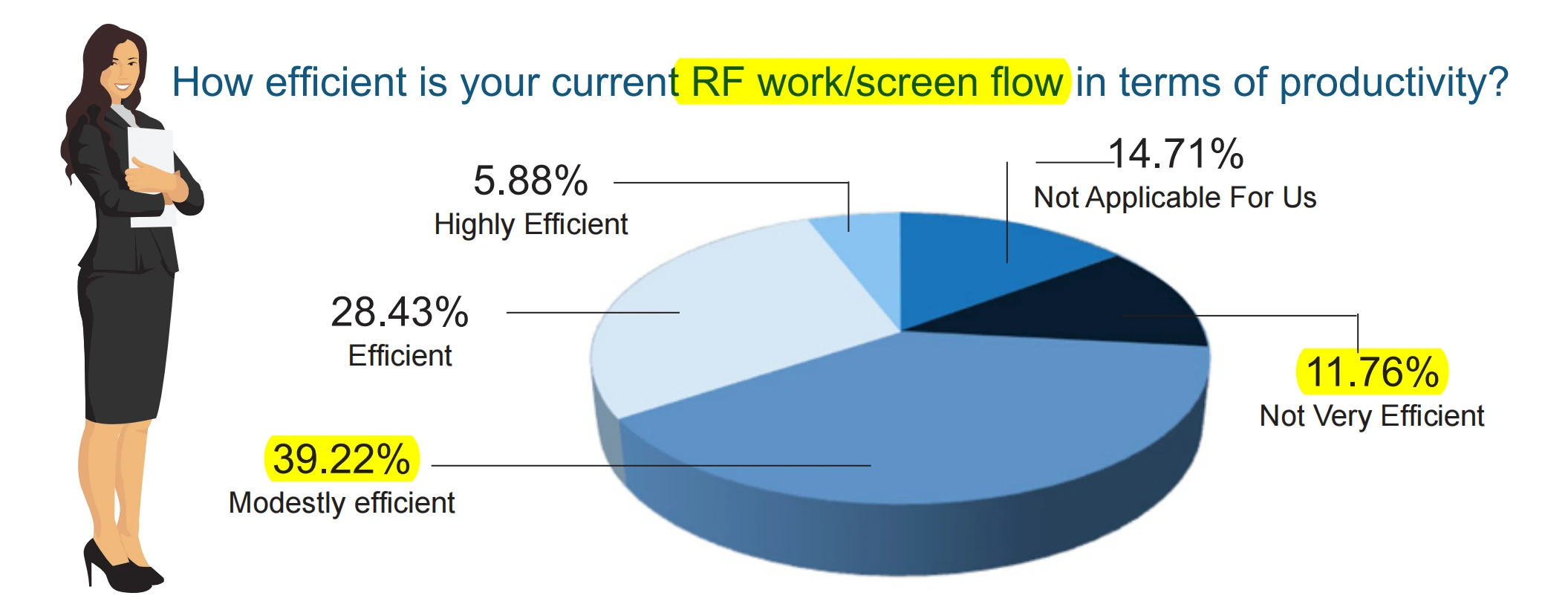

Almost half of the respondants believe that their DCs are "efficient", about more than 38% deemed low or average.

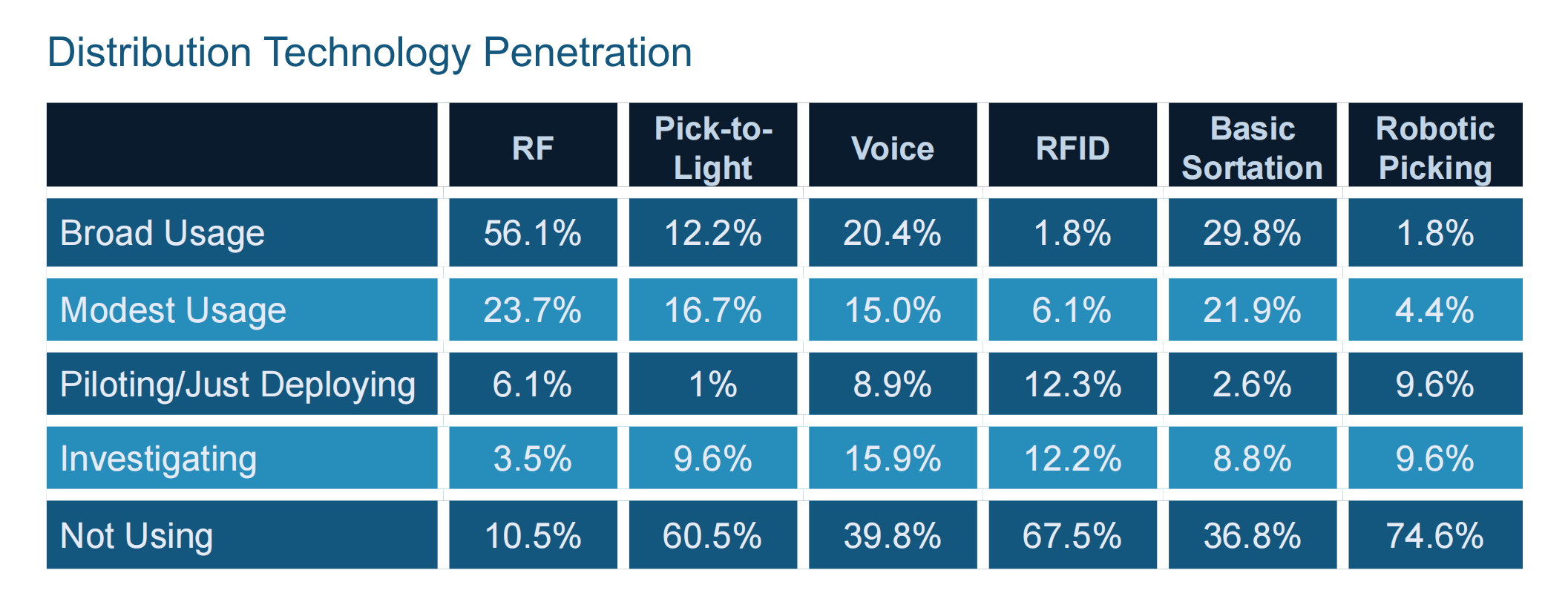

The subsequent section compares six different technologies and their applications. From broad application perspective or suitability, RF Scanner remains dominant. RFID and Robotic Picking are the minor players where RFID is still at infancy stage.

About 30% of participants use various technologies, where up to 40% still have not used any in their operations.

Pick-to-Light is unique. It is common for picking or retail operations (also for storage purpose). In terms of broad application among users, it has 12% shares.

Voice ranks after RF Scanner (20%-broad application and 15%-suitability). We believe Voice is gaining momentum. The outcome would even be lower if a survey was conducted five years prior to this one.

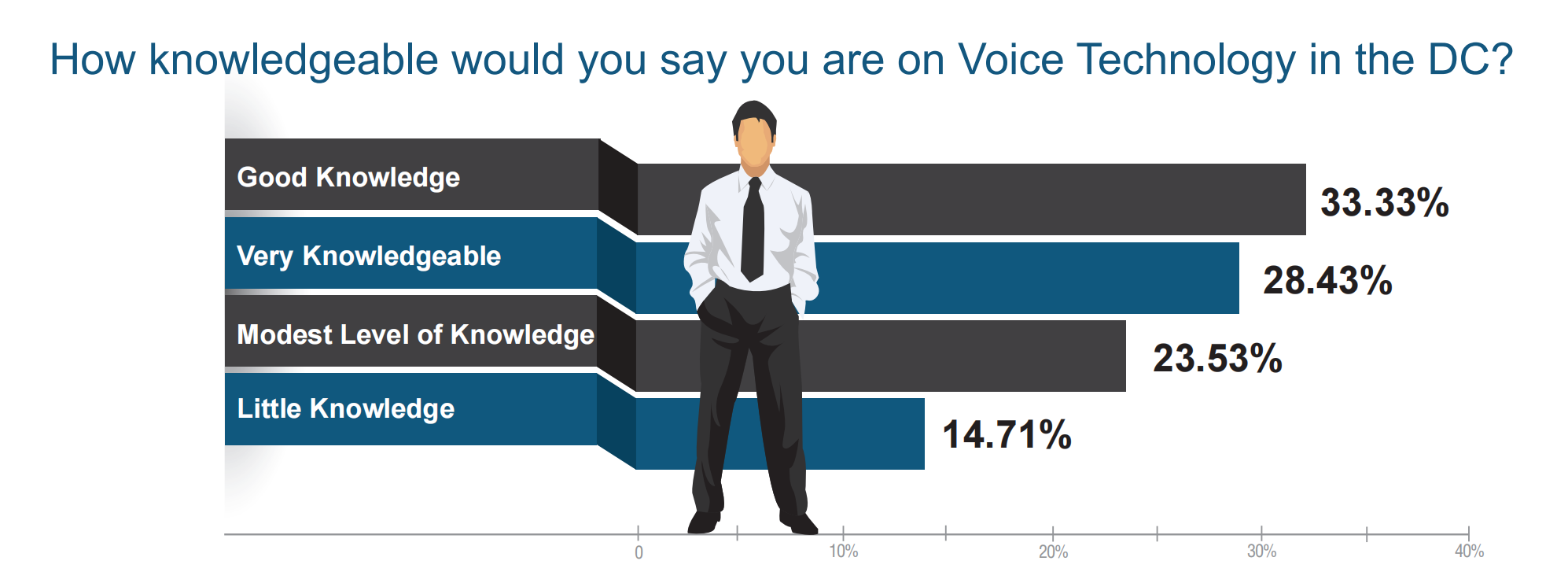

At the time of this study, more than 24% of the companies were assessing or implementing Voice.

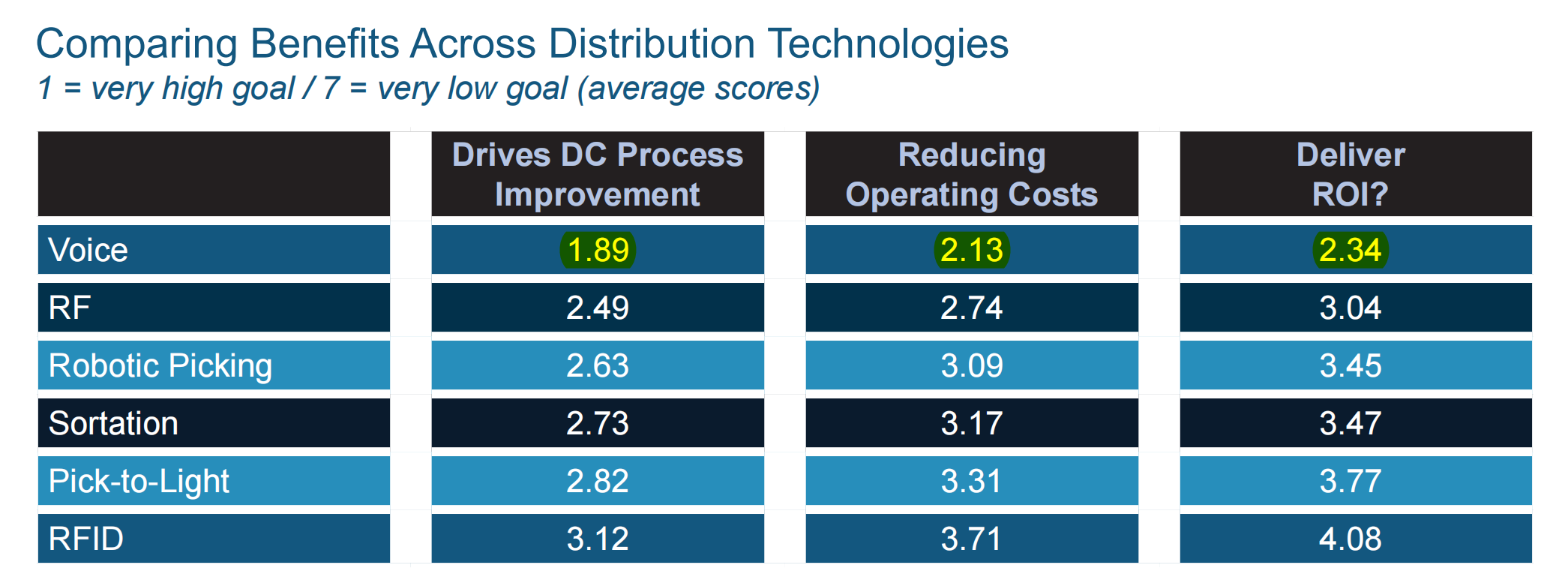

Another part of the survey was the competitive edge of each technology, Voice stands out among all on the three criteria assessed.

Although RF Scanner being placed at second, there was a significant gap as compared to Voice. Robotic Picking stood out in reducing operating cost and workflow improvement. However, users have concern on its ROI.

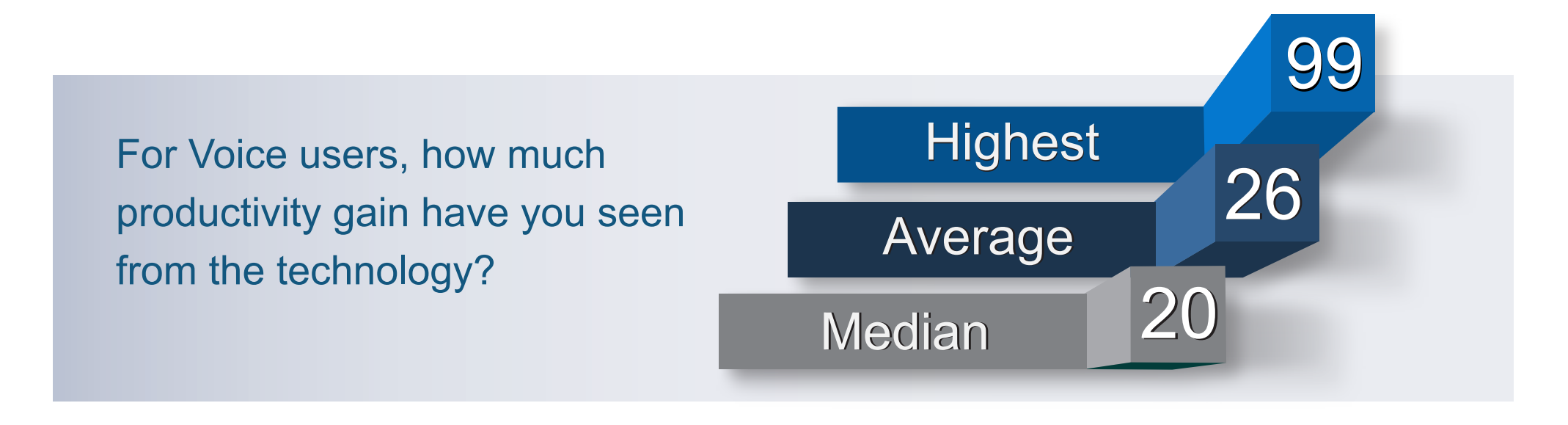

One of the focuses is on productivity gain upon voice implementation. From the chart, a very convincing fact was that the average gain is 26% where the median is 20%. On the extreme, one user has a 100% gain through voice.

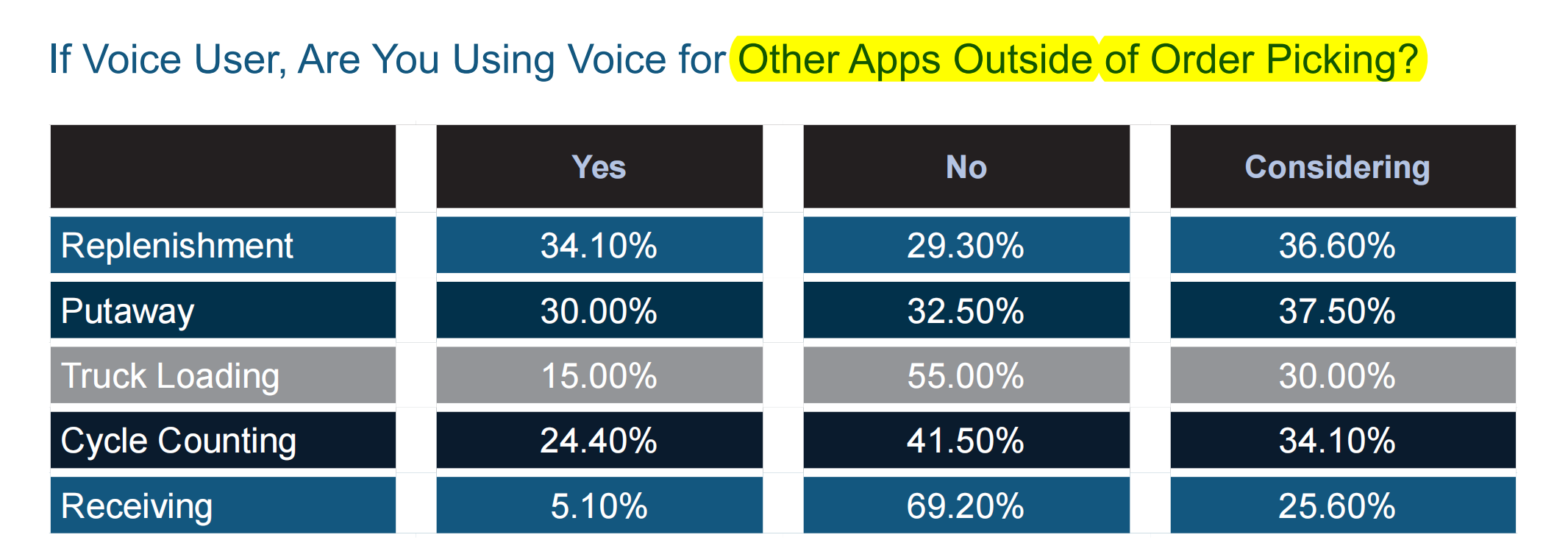

For Picking, voice remains competitive in terms of hands-free comparing with RF Scanner. Among the voice users from the survey, 34.1% and 24.4% use this technology for replenishment and cycle counting respectively. Voice application in receiving remains low.

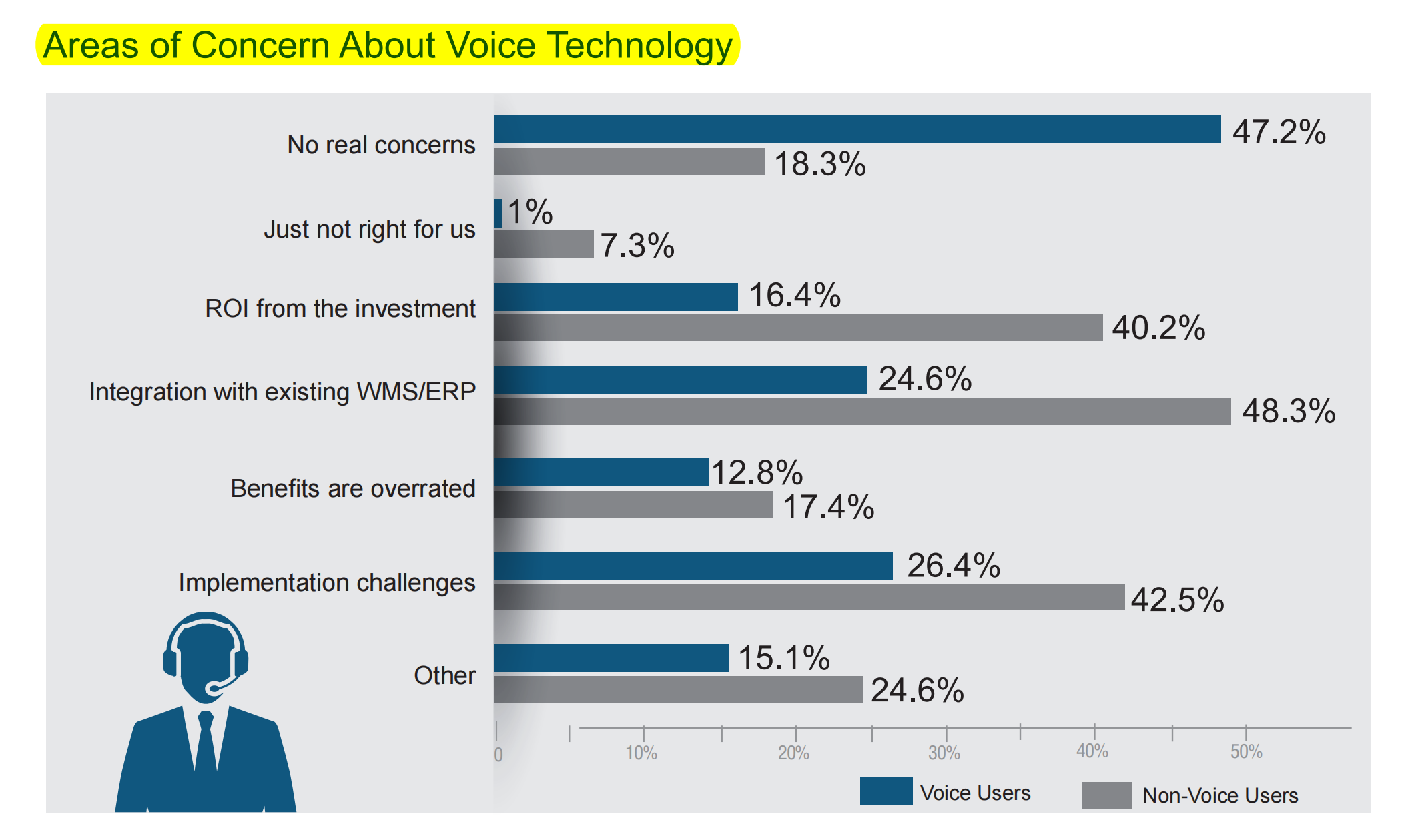

Next section looked into the concerns from Voice and non-Voice users. 47.2% of current voice user indicated that they have no cconcern on voice technology. This is significantly lower for non-Voice users. This indirectly implies a site visit to see Voice in action helps clear the doubt and provide reassurance on Voice's operability.

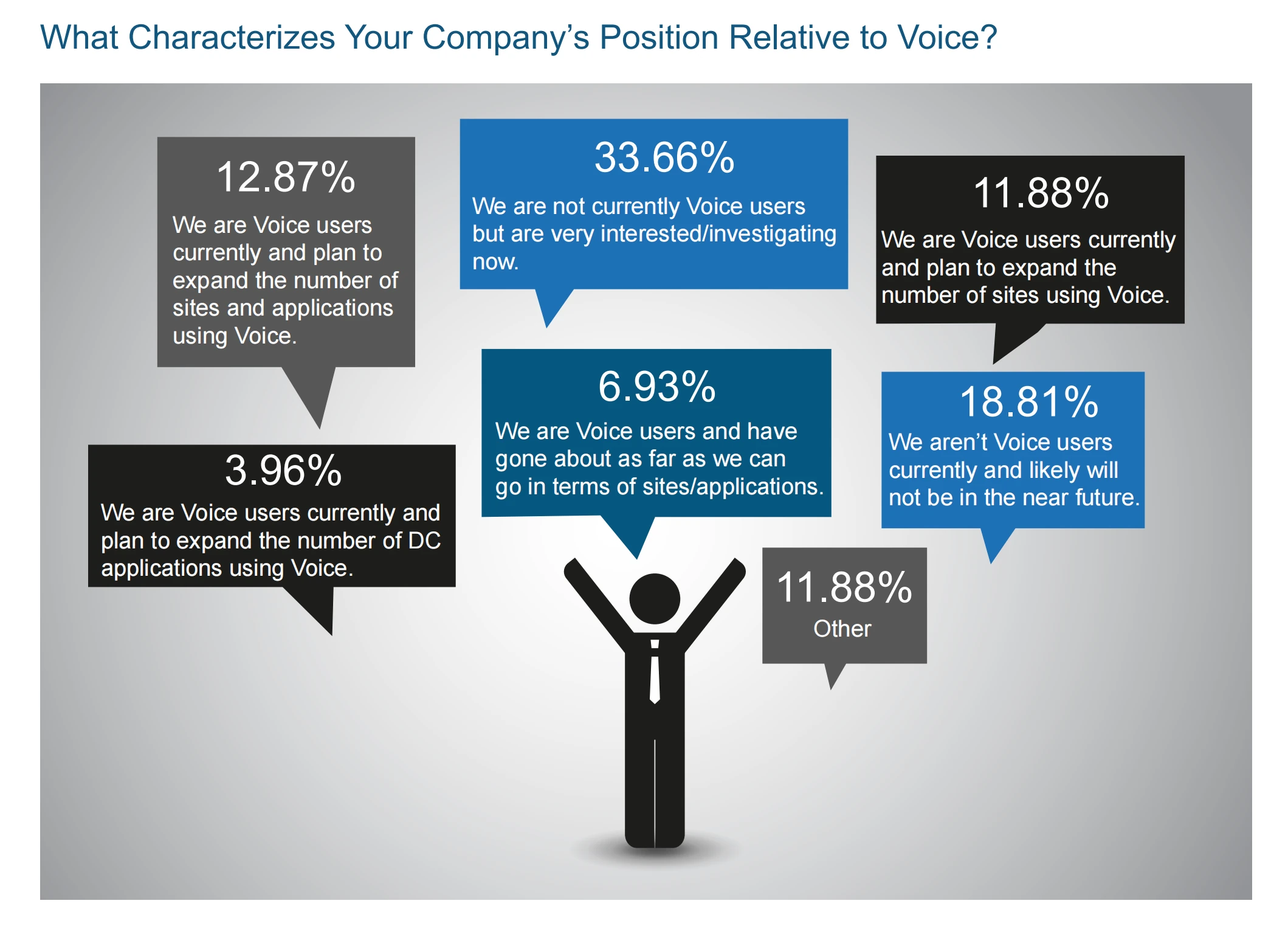

Voice service provider continues to address the enquiries on multi-lingual support, maintenance & support fees and user adaptibility to new workflow, just to name a few. Most of these are due to lack of understanding of the technology. 33% expressed the interest in moving to voice despite the fact that they have not implemented it where 18% said they are not a voice user now and will not consider it in the future.

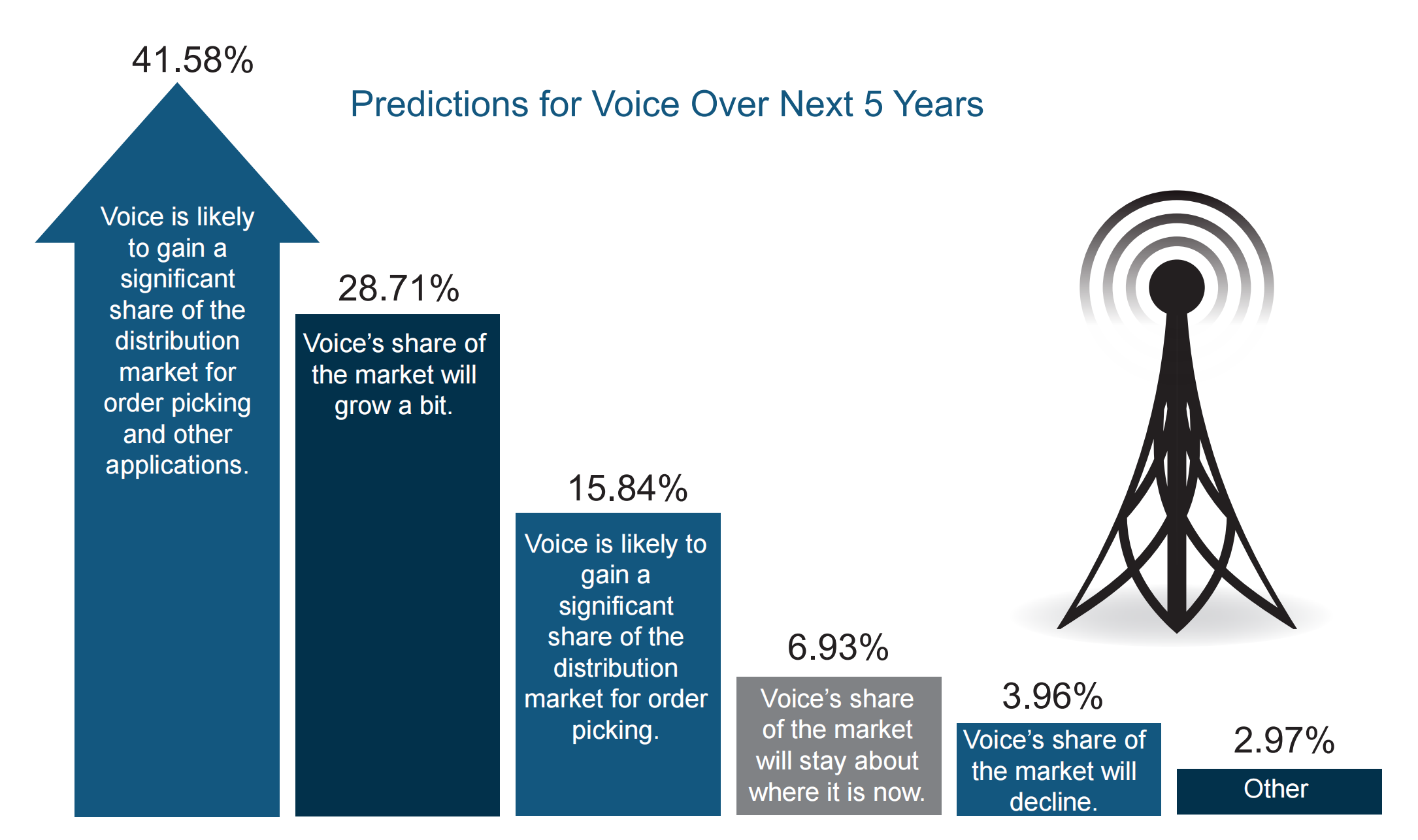

Many respondants see the prospect of Voice. 41.5% believes that it will continue to gain market shares. This includes extending the application to outside of picking. Only 4% anticipated a reduction.

Conclusion

Voice stands out among the six technologies in this survey. It has highest rating with respect to workflow improvement, cost reduction and ROI.

There are multiple technology options available for a DC. From this report, the focus is on infrastructure and physical setup instead of warehouse management system (WMS) or warehouse control system (WCS). A broad perspective is required when building a business case. A combination of could be the best for optimal efficiency such as batch picking and sortation system by leveraging on accuracy and hands-free of voice picking. The survey has clearly shown that voice continues to develop is due to its strengths in workflow enhancement, reducing operating cost and high ROI. Many current voice users are exploring the alternative of using voice in other warehouse applications. They have positive outlook on voice's future trend. We believe in the growth of voice's market share. New technologies such as RFID and Robotic Picking are still in their infancy stage. Time will tell when a new survey is conducted while emerging technology might appear on the list.